Update on the Economy and Investment Markets 10-30-21

Welcome to the Stearns Financial Fireside Chat.

It’s Halloween season, and one of the scariest scenarios our clients worry about is the future of U.S.-China relations. This is followed by the future of everything else! We talk about our future with China in this Chat’s frequently asked questions, below.

As for the future of everything else, you can refer to last week’s Live Chat where we hosted two futurists, Ryan Hodapp, CFA and Greg Stum, CFA, both at Resolute Managers. Ryan and Greg regularly collaborate with a network of interesting futurists, including the irrepressible Cathie Wood of Ark Invest and former head of Global Thematic Strategies at Alliance Bernstein.

We caught Ryan and Greg immediately following their presentation at the Schwab national conference (hosted virtually) where they conducted a lightening round of ideas on future technology themes.

Our Live Chat session with Ryan and Greg centered on Morningstar’s 9 future themes. One thing everyone agreed on – these 9 themes have moved into the deployment phase, in some cases accelerated by the pandemic-induced immediate “need for innovation”.

#1. Big Data and Analytics: This area includes capabilities with data sets too large and complex to manipulate or interrogate with standard methods or tools. Related subthemes include the “Internet of Things,” machine learning, and artificial intelligence.

Key takeaways:

- Obviously, big data and analytics is a key piece of the future as it ties into each of the other 8 themes. Example: 1 (big data) + 1 (networks) + 1 (medicine) = 10X, not 3X, the expected rate of innovation in medicine.

- Expect this area to be high impact for businesses of all kinds, providing a tailwind for both revenues and profit margins.

#2. Networks and Computer Systems: Technology leaps (ranging from hyperconnectivity and integrated systems to service continuity to new software-defined architectures) will have a massive impact on the way people think of connecting applications and software with hardware.

Key takeaways:

- This is still in the early innings according to our guest thought leaders. Hyperconnectivity creates accelerated, not linear, growth.

- Faster computers allow faster analysis of big data, and better decision-making capabilities.

#3. Nanotechnology: Another future trend is nanotechnology, that is, the branch of technology that deals with dimensions and tolerances of less than 100 nanometers, particularly the manipulation of individual atoms and molecules. We see a range of potential applications in this area spanning multiple disciplines, including medicine, computing, manufacturing, and travel.

Key takeaways:

- Our guest thought leaders are not as deep into nano, but their passing knowledge suggested “big things from little atoms” in the future. They mentioned quantum computing, believing it will be super powerful but still 10+ years over the horizon.

- Other thought leaders in the nano space believe many new breakthroughs in materials, including battery technology, will be led by nano.

#4. Medicine and Neuroscience: Sciences, such as neurochemistry and experimental psychology, that deal with the nervous system and brain is another of Morningstar’s 9 themes. Key advancements in unlocking the human genome have created an infrastructure of biomarkers, while paradigm shifts in biotechnology that can alter the immune system are radically changing the way we treat diseases.

Key takeaways:

- Our expert guests focused on precision medicine and the ability for faster, cheaper human genome mapping to allow more targeted medicine therapies, increasing both safety and effectiveness in the future.

- Ironically, but unsurprisingly, our guests were mixed in their views on how technology disruption would affect government health care initiatives in the next decade. Many government policy experts concede that a large portion of future health care improvements will be driven by the private sector, not the federal government. Pricing via Medicare, however, does matter and the federal government controls those purse strings.

#5. Energy and Environmental Systems: This area involves the exploration of renewable energy sources such as solar, wind, water, and batteries. As organizations continue to establish processes to help reduce negative environmental impacts and increase operating efficiencies, new technological advancement across sectors will emerge.

Key takeaways:

- Our thought leader guests believe that alternative energy technologies are moving fast enough to make them fully competitive with fossil fuels by 2025.

- They and other SFG research sources also believe the current energy crisis happening around the world is the result of poor transition planning on the part of governments trying to rush along the changeover from fossil fuels to renewable sources even as post-pandemic energy demands are soaring.

#6. Robotics: As the name implies, robotics is the branch of technology that deals with the design, construction, operation, and application of robots. Advances in robotics, specifically when combined with other technologies, have potentially infinite applications, spanning technology, industrial, medical, and consumer-facing channels.

Key takeaways:

- This area promises “explosive” potential growth, with human and robot teams considered by many to be the main growth area over the next decade.

- Again 1 (robotics) + 1 (artificial intelligence) + 1 (advanced computer networks) will create exponential productivity increases in the coming decade.

#7. 3D Printing: 3D printing is a process for making a physical object from a digital file – i.e. “printing” it into a 3D object. The emerging trend is ready for mainstream consumption and has ample potential to disrupt several industries, from industrial manufacturing and medicine, to consumer products and retail.

Key takeaways:

- Early 3D results were disappointing in many areas while the “frenzy” stage culminated.

- The deployment phase, however, is looking very strong, especially as manufacturers of all types look for ways to make things closer to home, relying less on long supply chains.

- Our guests mentioned aeronautics (commercial and military) as strong future users of 3D printing for parts.

#8. Bioinformatics: The science of collecting and analyzing complex biological data is yet another of the 9 themes – one that has the potential to positively affect both the duration and quality of human life.

Key takeaways:

- The more we know about our own unique biology and predictive DNA, the better we can maintain good health and move more towards the realm of true wellness rather than the simply focusing on the absence of illness.

#9. Financial Innovation: It’s no surprise that our evolving global economy has spurred a search for, and acknowledgement of, emerging funding sources, platforms, currencies, and stored and transferred value. In other words, no longer do we think only about opportunities to expand production. We think also about the underlying currencies used (including cryptocurrencies), as well as structural shifts in technology and payment delivery methods, which includes blockchain.

Key takeaways:

- Our guests support the emerging trends in blockchain and cryptocurrencies. They reinforced that this is another area in the early innings, and direct investments should be made with care and with the recognition that some of these areas are in the highly volatile “frenzy” stage.

- They also believe that established financial entities, like big banks, are going to have trouble with the massive disruption and competition coming from non-bank areas.

Here are some specific examples of some of these trends, and how combining trends together can create “super turbocharged results”. https://www.mercuryds.com/blog/7-emerging-trends-in-ai

SFG’s Take: Most of these future trends are very positive for humanity and for companies who get it right. Getting it right is obviously the hard part, as each of these trends require an investment in the future, an ability to change well, and a need to hit the market at the right time.

There are also downsides to some of these technologies, including cyber-hacking and privacy issues. Job displacement is a downside, but that has been the case in the U.S. for over a century – each of the 3 previous industrial revolutions have created severe job displacement and have required the retraining of workers. The current revolution is shifting jobs faster, although some of our super trend network has pointed out that retraining tools have never been better for those who actually want to get retrained.

We view many direct investments in these areas as “explore” (higher risk, potentially higher return) options. Many of SFG’s top 20 companies across our firm in “core” positions are already positioning themselves to benefit from these future trends.

KEY POINTS TO CONSIDER

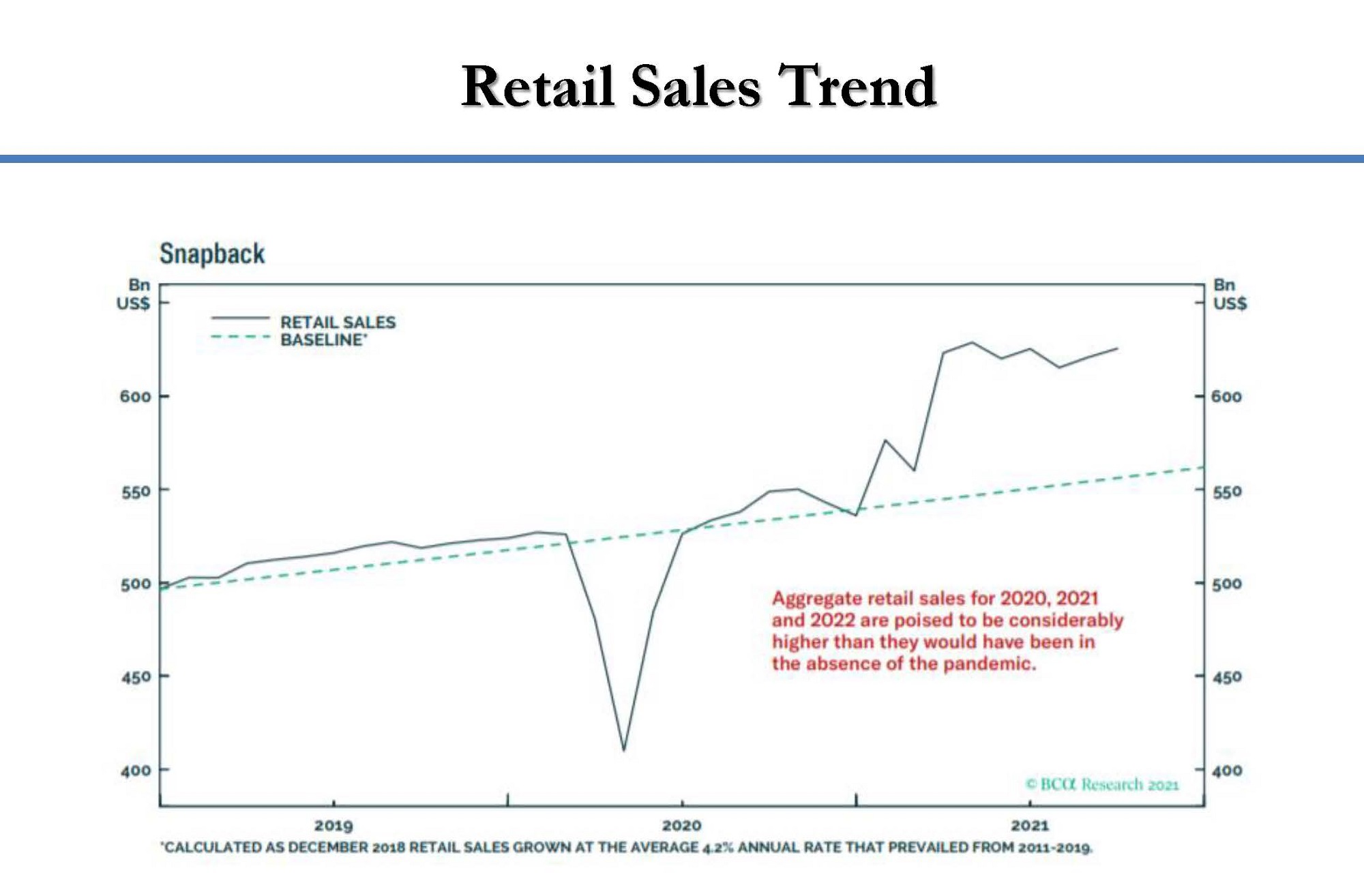

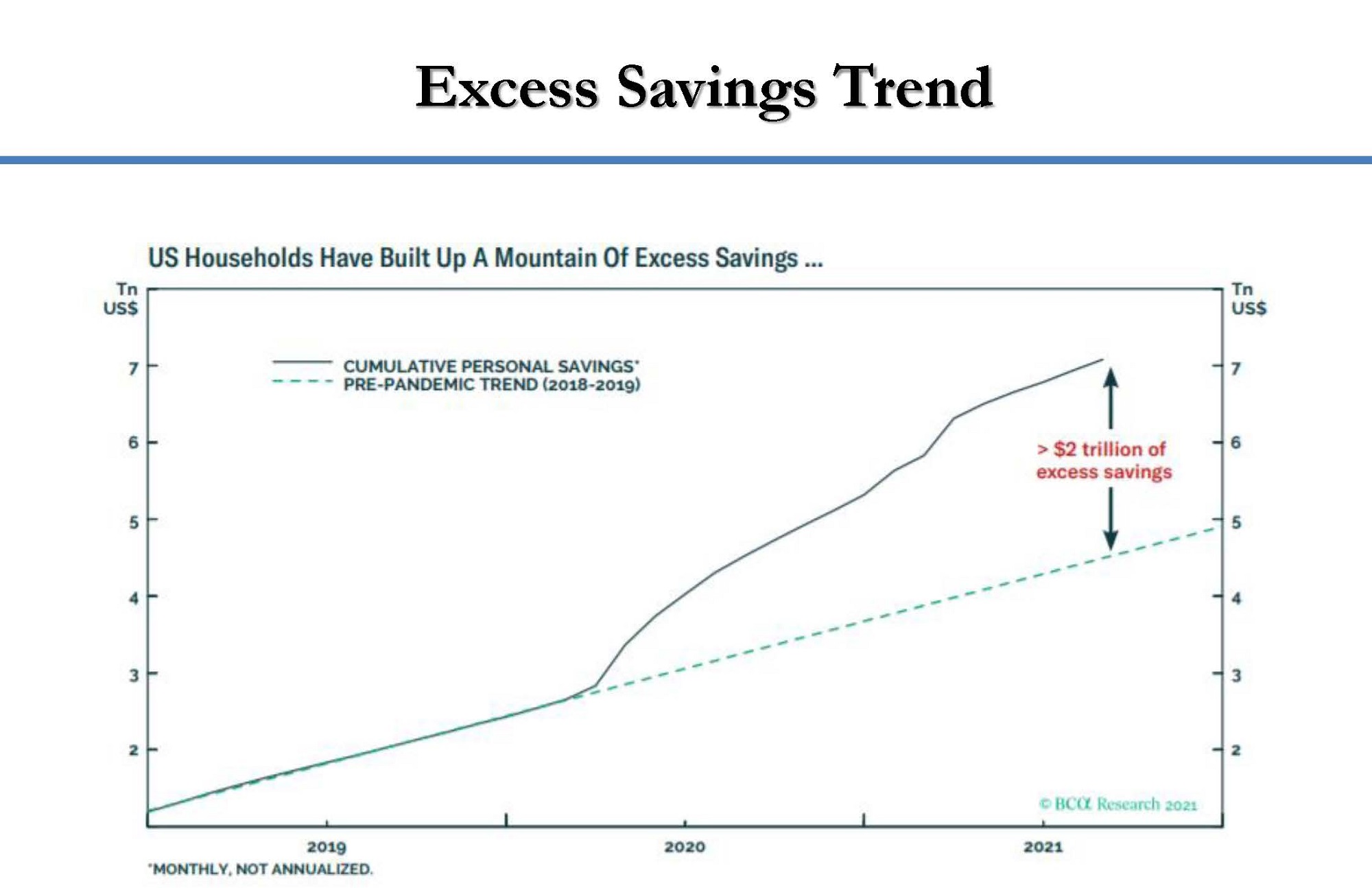

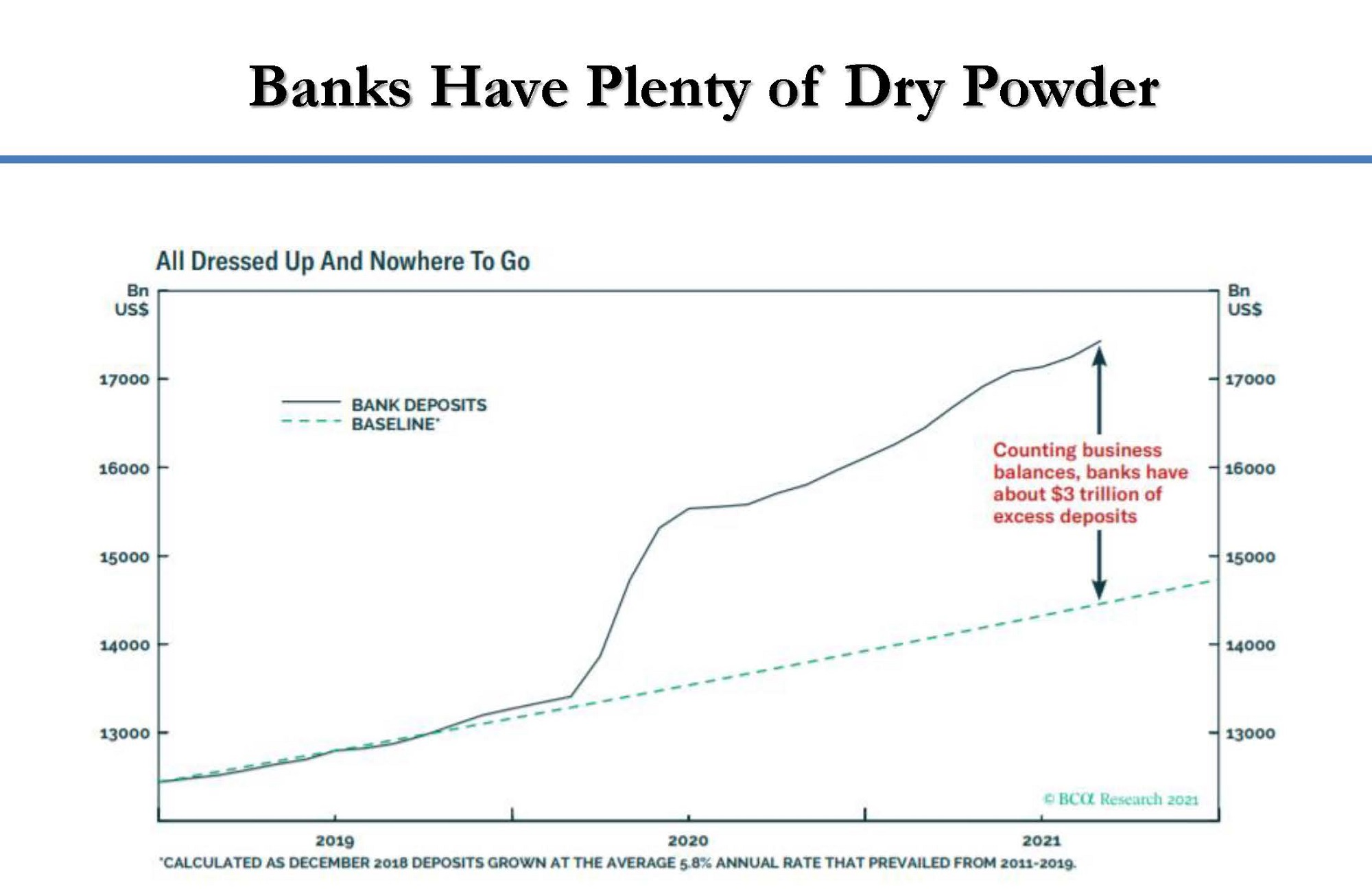

➢The following 3 charts sum up key trends that bode well for continuing economic growth in the U.S. in 2022 despite slow downs caused by supply chain bottlenecks.

SFG THOUGHT LEADERSHIP

➢Investing in Opportunity Zones Could Compliment a Diversified Retirement Income Strategy

Dennis Stearns, CFP provides considerations and risks associated with investing in opportunity zones; a strategy for deferring capital gains taxes.

Read the full article here: https://wealthpop.com/retirement-investor/investing-in-opportunity-zones-could-compliment-a-diversified-retirement-income-strategy

➢Here Is Everything You Need to Know About ESG: A Socially Responsible Way of Investing

Haleh Moddasser, CPA contributes to this article which summarizes the history, evolution and current strategies associated with aligning investments with values.

Read the full article here: https://time.com/nextadvisor/investing/investing-in-esg/

FREQUENTLY ASKED QUESTIONS

Questions on China

Q: Should we be concerned about China invading Taiwan? It seems that China is pushing on many fronts to force Taiwan back into the fold.

A: The risks are the highest they have been in decades that China will attempt to fold Taiwan back into mainland China. Any “war” is probably not going to look like most imagine. For example, China has engaged in more modern “asymmetric” strategies, including cyberwarfare, thereby creating political instability in Taiwan. We can’t rule out a more traditional conflict that perhaps pulls the U.S. and its allies into a broader conflict, though this eventuality seems less likely.

So far, the potential for downside risk, including economic loss, has deterred the Chinese from pushing beyond the brink. China must consider, for example, what Apple CEO, Tim Cook, would do with its supply chain in China if outright war broke loose. Is this a risk China can take?

While it’s true that economic ties with China have been strained in recent years (not helped by the pandemic), the U.S. & China still have significant trade with one another that makes a potential invasion of Taiwan more daunting for China.

SFG’s Take: Most geopolitical events, threatened or actual, are rarely actionable from an investment viewpoint. Many of our clients are not happy with recent Chinese provocations, but most want to have some investment in the largest infrastructure project in the history of the world – that is, the “new and improved” Chinese belt and road initiative. At SFG, we are investing in China less directly by investing in European companies that support the project, though we do have some direct exposure to China in our more aggressive growth emerging market funds.

The risks surrounding China underscore the importance of clearly defining and understanding the “core” versus “explore” strategies within your portfolio. Having a balanced portfolio, and some stable (albeit unexciting) assets for more conservative investors, still makes sense even in this age of low interest rates.

Here is a good sampling of Chinese experts on U.S.-China policy: https://www.foreignaffairs.com/ask-the-experts/2021-10-19/us-foreign-policy-too-hostile-china

For more historical context on U.S.- China relations: https://www.cfr.org/timeline/us-relations-china

Q: Should we be concerned about Chinese debt toppling the world economy?

A: Probably not. There has been concern that the Chinese real estate developer Evergrande Group could default on many bonds and that would cause other developers around the world to face investor sell-offs.

GaveKal, one of SFG’s research sources, believes the current financial stress on property developers is due in large part to a regulatory campaign by the Chinese to cool down the property market and force developers to deleverage (pay down debt). The only thing that will greatly reduce the odds of more developer defaults is a material reversal in this policy.

Investors have dumped offshore bonds of Chinese property developers since Evergrande began missing debt payments in late September. The sell-off deepened in October as other developers also missed payments or asked for extensions, raising expectations of widespread defaults in the property sector.

The default worries have effectively shut down the offshore bond market for Chinese developers. With average yields on their dollar bonds now around 20%, it has become prohibitively expensive to refinance offshore debt, and new issuance has ground to a halt.

With that said, market sentiment recovered somewhat last week after Evergrande made a bond payment. After reports that it had successfully made the $83.5M offshore interest payment, prices of offshore developer bonds recovered further, and Chinese equities rallied.

Thanks to the payment, a formal default by Evergrande—which would trigger “cross-defaults” on other bonds it had issued or guaranteed—has been postponed. But making one payment does not mean the wave of developer defaults is over, or that the freeze in demand for developer debt has thawed.

Last week’s payments make it clear that Evergrande is trying to avoid default for as long as possible. However, it still has another $683M in dollar denominated offshore and onshore interest payments due this year. Evergrande last week reported it had not made any progress in selling assets, and that its housing sales tumbled in September.

China’s property developers are experiencing their worst funding squeeze in years, as banks cut lending, new bond issues dry up and proceeds from property sales decline. The financial strains on developers are serious and go far beyond one firm’s management problems.

Developers including Fantasia Holdings, China Properties Group and Sinic Holdings have missed payments this month, and last week Modern Land dropped an attempt to negotiate a three-month interest extension, triggering concerns it will also default.

The missed payment by Fantasia in early October was perhaps most troubling to investors, as it appeared to have enough cash on hand to make the interest payments. Investors are concerned developers could selectively default on offshore debt, although Evergrande has so far avoided that course.

The incentives are nonetheless not favorable for offshore bond holders. Because the offshore bond market is relatively small, it is more important for developers to maintain their access to the onshore bond market and domestic bank lending. It would be rational for developers with limited funds to prioritize paying back onshore creditors.

Chinese policymakers have taken steps to ensure developers get the funds they need to finish their ongoing projects, so they can deliver housing to the households who have paid for it.

The conservative policy framework in China expressed by the slogan “housing is for living in, not for speculating” remains in place.

Last week’s announcement by the Chinese National People’s Congress of a five-year program to test a new property tax further underscores how the policy environment in China is shifting. In Gavekal’s opinion, with sentiment already poor, the tax announcement will likely further weigh on sales and prices.

SFG’s Take: We rate these developments as worthy of monitoring, but don’t believe the debt concerns are a contagion that will spill over into worldwide real estate debt markets. SFG currently has no holdings in China exposed to this high risk/high yield sector.

SUMMARY

Future technology trends have been accelerated by the pandemic and remain mostly positive in a host of areas, including energy, health care and the productivity of workers and companies in the U.S. and abroad. Whether the volatility of some of the targeted investments in this area is worth the potential gains is an “explore” issue unique to each of our clients. Fortunately, SFG’s top holdings are all heavily engaged in many of the 9 future trends profiled.

SFG’s three pillars of recovery remain in positive trend territory. Wildcard risks discussed in this and previous Chats remain, including the China-Taiwan scenarios discussed in this Chat.

SFG is balancing numerous opportunities and threats in our portfolios, customized to our clients’ unique circumstances.

In growth portfolios, we are leaning into a variety of short- and intermediate-term asset classes and trends that we believe have favorable forward-looking risk/reward relationships.

In more conservative growth and income portfolios, we are maintaining good diversification while striving for positive real returns over inflation.

Our COVID-19 investing approach can be summed up by six themes:

- Diversification with a balance of offensive and defensive measures, depending on the desired risk tolerance of our clients,

- Underweighting, or avoiding areas of higher future concern,

- A focus on higher-quality investment themes,

- Identifying and implementing buying opportunities that may be appropriate for more growth-oriented portfolios,

- A more defensive stance using different portfolio tools for more conservative growth and income portfolios, and,

- Utilizing select alternatives to traditional bonds and stocks.

~ Dax, Dennis, Glenn, Jason, John and PJ

(the SFG Investment Committee)

Stearns Financial Group is a group comprised of investment professionals registered with Hightower Advisors, LLC, an SEC registered investment adviser. Some investment professionals may also be registered with Hightower Securities, LLC (member FINRA and SIPC). Advisory services are offered through Hightower Advisors, LLC. Securities are offered through Hightower Securities, LLC.

This is not an offer to buy or sell securities, nor should anything contained herein be construed as a recommendation or advice of any kind. Consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. No investment process is free of risk, and there is no guarantee that any investment process or investment opportunities will be profitable or suitable for all investors. Past performance is neither indicative nor a guarantee of future results. You cannot invest directly in an index.

These materials were created for informational purposes only; the opinions and positions stated are those of the author(s) and are not necessarily the official opinion or position of Hightower Advisors, LLC or its affiliates (“Hightower”). Any examples used are for illustrative purposes only and based on generic assumptions. All data or other information referenced is from sources believed to be reliable but not independently verified. Information provided is as of the date referenced and is subject to change without notice. Hightower assumes no liability for any action made or taken in reliance on or relating in any way to this information. Hightower makes no representations or warranties, express or implied, as to the accuracy or completeness of the information, for statements or errors or omissions, or results obtained from the use of this information. References to any person, organization, or the inclusion of external hyperlinks does not constitute endorsement (or guarantee of accuracy or safety) by Hightower of any such person, organization or linked website or the information, products or services contained therein.

Click here for definitions of and disclosures specific to commonly used terms.